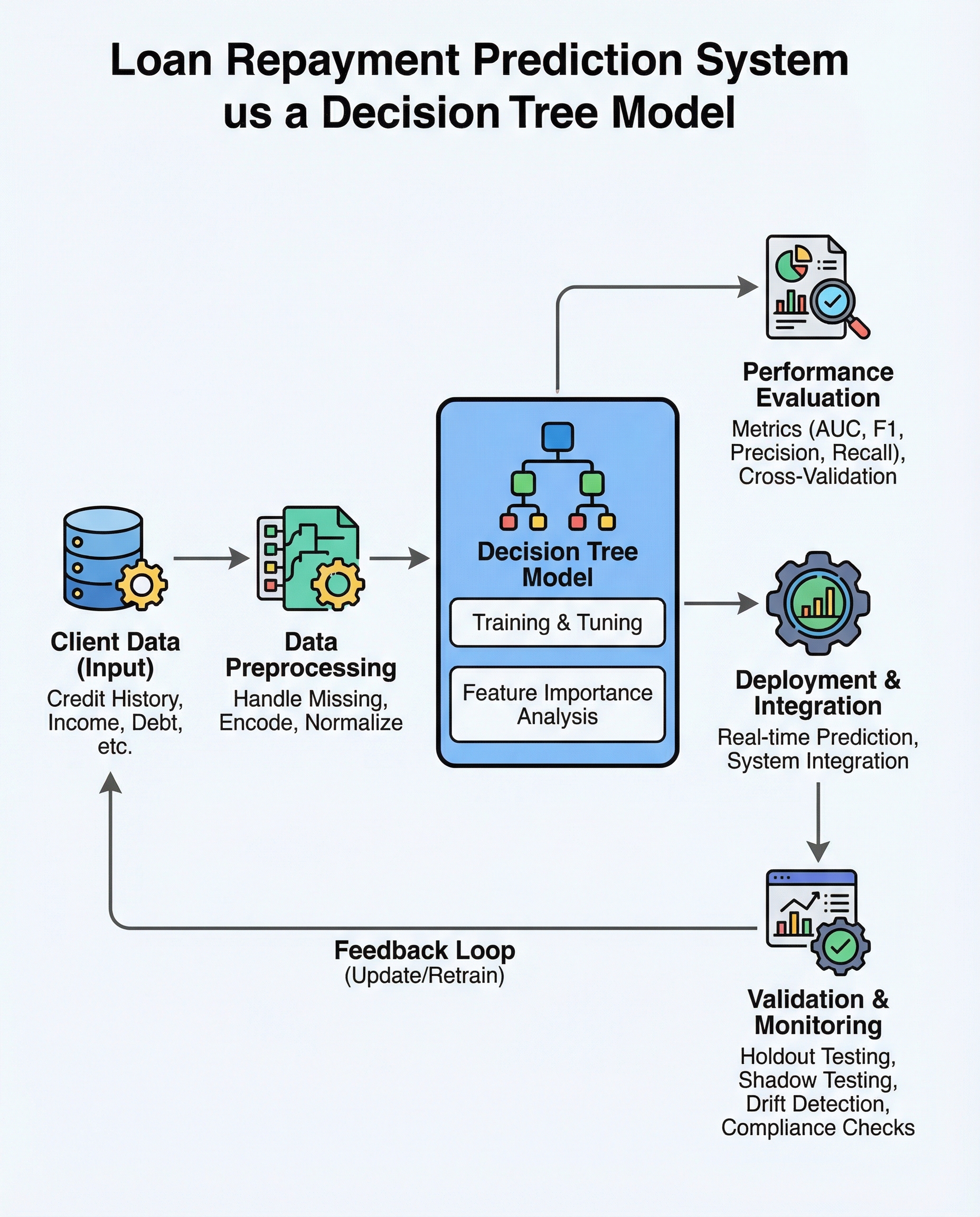

Decision Trees in Loan Repayment: Stop Using Accuracy as Your “Effectiveness” Metric

bugfree.ai is an advanced AI-powered platform designed to help software engineers master system design and behavioral interviews. Whether you’re preparing for your first interview or aiming to elevate your skills, bugfree.ai provides a robust toolkit tailored to your needs. Key Features:

150+ system design questions: Master challenges across all difficulty levels and problem types, including 30+ object-oriented design and 20+ machine learning design problems. Targeted practice: Sharpen your skills with focused exercises tailored to real-world interview scenarios. In-depth feedback: Get instant, detailed evaluations to refine your approach and level up your solutions. Expert guidance: Dive deep into walkthroughs of all system design solutions like design Twitter, TinyURL, and task schedulers. Learning materials: Access comprehensive guides, cheat sheets, and tutorials to deepen your understanding of system design concepts, from beginner to advanced. AI-powered mock interview: Practice in a realistic interview setting with AI-driven feedback to identify your strengths and areas for improvement.

bugfree.ai goes beyond traditional interview prep tools by combining a vast question library, detailed feedback, and interactive AI simulations. It’s the perfect platform to build confidence, hone your skills, and stand out in today’s competitive job market. Suitable for:

New graduates looking to crack their first system design interview. Experienced engineers seeking advanced practice and fine-tuning of skills. Career changers transitioning into technical roles with a need for structured learning and preparation.

Decision Trees in Loan Repayment: Stop Using Accuracy as Your “Effectiveness” Metric

When predicting loan repayment, the word “effective” shouldn't be equated with “high accuracy.” For imbalanced problems—where most customers repay and only a few default—a model that always predicts "repay" can easily reach 90%+ accuracy and still be useless.

Why accuracy fails

- Accuracy treats every mistake equally. In lending, a missed defaulter (false negative) and wrongly rejecting a good borrower (false positive) usually have very different business costs.

- Example: If 95% of customers repay, a model that predicts "repay" for everyone scores 95% accuracy but catches zero defaulters.

Metrics you should insist on

Tie the metric to business impact. In interviews and model evaluations, prefer cost-aware and class-sensitive metrics:

- Recall (sensitivity) for defaulters: how many actual defaulters the model catches. Use this to reduce false negatives.

- Precision for defaulters: of those flagged as likely to default, how many actually default. Use this to avoid rejecting too many good customers.

- F1 score: harmonic mean of precision and recall to balance the two when you need a single number.

- AUC-ROC: measures ranking quality across thresholds; useful but can be misleading with heavy class imbalance.

- PR-AUC (Precision-Recall AUC): often more informative than ROC when defaults are rare because it focuses on the positive (default) class.

Also evaluate calibration (do predicted probabilities match actual rates?) so you can set meaningful business thresholds.

Always connect metrics to business loss

Define a cost matrix: specify the loss (in dollars or business impact) for false negatives and false positives. Then:

- Optimize expected business loss (or a profit/loss metric) rather than raw accuracy.

- Choose the threshold that minimizes expected loss or meets a risk policy constraint (e.g., max allowable portfolio default rate).

This turns model evaluation into a business decision, not a modeling vanity contest.

Practical evaluation checklist

- Compute a confusion matrix on a holdout/test set.

- Report recall, precision, F1, ROC-AUC and PR-AUC; include calibration plots.

- Translate false positives/negatives into monetary (or operational) cost and compute expected loss per threshold.

- Use stratified cross-validation for stable estimates with imbalanced classes.

- If needed, use class weighting, resampling, or thresholding—not accuracy—to address imbalance.

- Monitor model performance and business KPIs after deployment; distribution shifts can change the optimal threshold.

Interview tips

- Ask what the business cares about: cost per default, cost to acquire/lose customers, or regulatory limits.

- Show how you'd convert model outputs to a decision policy (thresholds, accept/reject rules) based on expected loss.

- Present ROC and PR curves, plus calibration, and recommend a threshold with its expected business impact.

Bottom line

Accuracy is easy to compute but often meaningless for loan-repayment models with imbalanced outcomes. Use recall, precision, F1, PR-AUC, calibration and—crucially—cost-based metrics that reflect business loss and risk policy. Insist on those in interviews and in production.

#MachineLearning #DataScience #MLOps