5 Fintech System Design Patterns Interviewers Expect You to Know

bugfree.ai is an advanced AI-powered platform designed to help software engineers master system design and behavioral interviews. Whether you’re preparing for your first interview or aiming to elevate your skills, bugfree.ai provides a robust toolkit tailored to your needs. Key Features:

150+ system design questions: Master challenges across all difficulty levels and problem types, including 30+ object-oriented design and 20+ machine learning design problems. Targeted practice: Sharpen your skills with focused exercises tailored to real-world interview scenarios. In-depth feedback: Get instant, detailed evaluations to refine your approach and level up your solutions. Expert guidance: Dive deep into walkthroughs of all system design solutions like design Twitter, TinyURL, and task schedulers. Learning materials: Access comprehensive guides, cheat sheets, and tutorials to deepen your understanding of system design concepts, from beginner to advanced. AI-powered mock interview: Practice in a realistic interview setting with AI-driven feedback to identify your strengths and areas for improvement.

bugfree.ai goes beyond traditional interview prep tools by combining a vast question library, detailed feedback, and interactive AI simulations. It’s the perfect platform to build confidence, hone your skills, and stand out in today’s competitive job market. Suitable for:

New graduates looking to crack their first system design interview. Experienced engineers seeking advanced practice and fine-tuning of skills. Career changers transitioning into technical roles with a need for structured learning and preparation.

5 Fintech System Design Patterns Interviewers Expect You to Know

Fintech systems must be correct, resilient, auditable, and low-latency. Interviewers often look for candidates who can name useful architectural patterns and, more importantly, explain the trade-offs and mitigations. Below are five patterns you should be ready to discuss, with why they matter, common pitfalls, and quick interview tips.

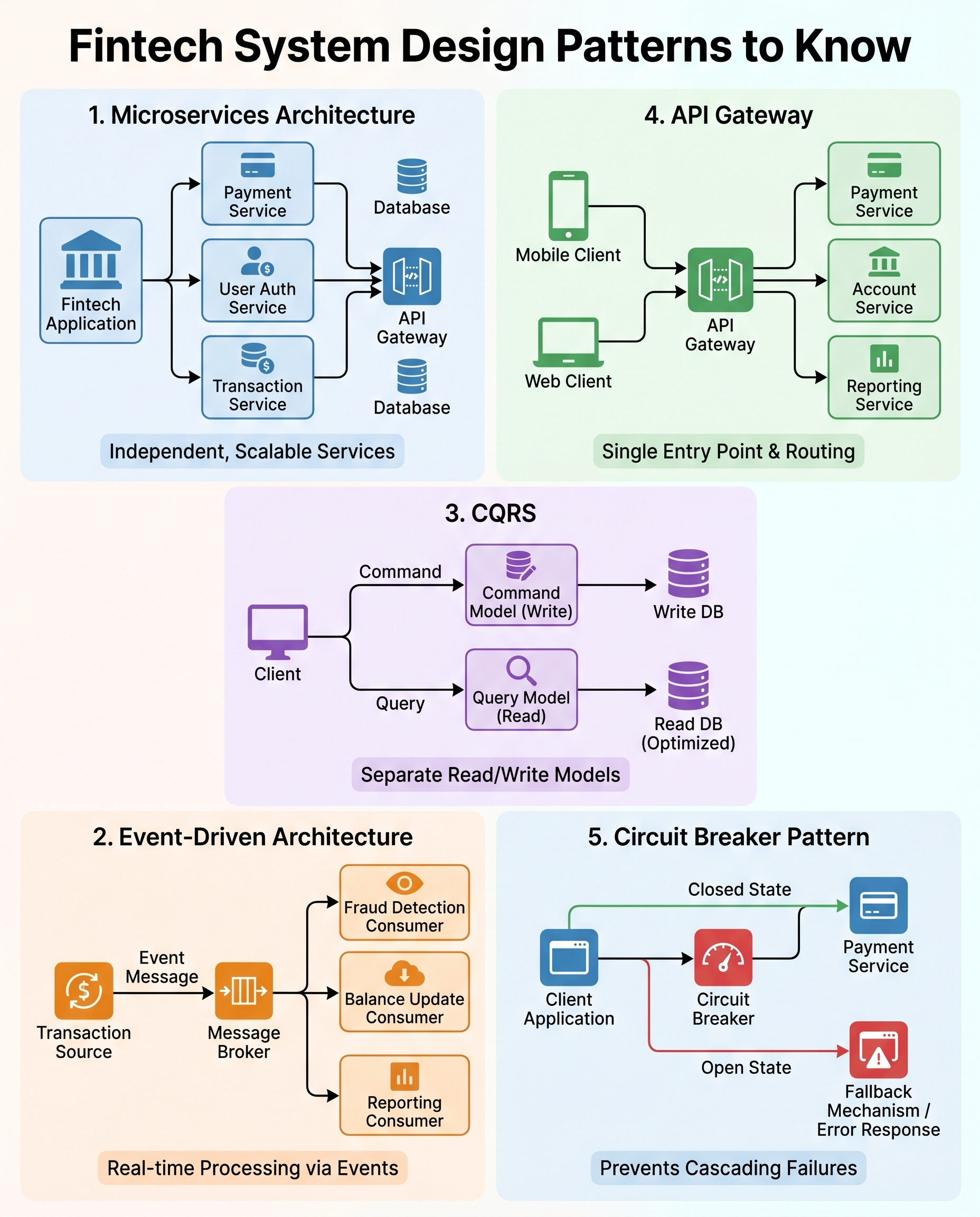

1) Microservices

What it is: Decompose a monolith into services by bounded context — e.g., payments, authentication, ledger, risk, notifications.

Why use it in fintech:

- Independent scaling per domain (peak payments vs peak reporting)

- Faster, safer releases and team autonomy

- Clear ownership for compliance & auditing

Trade-offs & mitigations:

- Distributed transactions: avoid two-phase commit; use sagas or event compensation patterns.

- Data duplication and consistency: define clear data ownership and use reliable event propagation or CDC.

- Operational complexity: invest in CI/CD, service discovery, observability (traces, logs, metrics) and service mesh when needed.

Interview tip: Describe the bounded contexts you’d pick for payments vs ledger, and how you’d enforce a single source of truth for balances (e.g., ledger service owns authoritative writes; other services subscribe to events).

2) Event-Driven Architecture

What it is: Use events and message brokers (Kafka, Kinesis, RabbitMQ) to decouple producers and consumers.

Why use it in fintech:

- Real-time processing for transactions, fraud detection, notifications

- Loose coupling and replayability for auditing and reprocessing

- Natural fit for workflows and asynchronous integrations

Trade-offs & mitigations:

- Ordering & delivery semantics: design for at-least-once delivery, make consumers idempotent, use partitioning keys for ordering when required.

- Processing guarantees: consider exactly-once semantics where necessary (e.g., Kafka with idempotent producers and transactional writes), but understand complexity.

- Operational costs: retention, compaction, and consumer lag monitoring are necessary.

Interview tip: Explain how you’d use events for a new payment: payment-created → ledger-updated → notification-sent → fraud-analysis, and how you’d handle retries and reconciliation.

3) CQRS (Command Query Responsibility Segregation)

What it is: Separate write models (commands) from read models (queries). Writes are processed by a command model, and one or more read-optimized projections are maintained for queries.

Why use it in fintech:

- Optimizes complex read patterns (dashboards, reports) independently of write throughput

- Read models can be denormalized for fast queries and scaled differently

- Works well with event sourcing for auditability

Trade-offs & mitigations:

- Eventual consistency between write and read models: make it explicit in APIs and provide reconciliation endpoints when strong consistency is required.

- Complexity of maintaining projections and migrations: add robust rebuild and versioning strategies for read models.

- Not always necessary: avoid premature use; start simple unless read or write scaling demands it.

Interview tip: When asked, outline where eventual consistency is acceptable (transaction history view) and where it is not (authoritative balance queries). Offer patterns for getting near-real-time guarantees (sync lookup fallback, monotonic reads, or read-through caching).

4) API Gateway

What it is: A single entry point that routes requests to backend services, handles authentication, rate-limiting, TLS termination, and sometimes request aggregation.

Why use it in fintech:

- Centralizes auth, request validation, and rate limits (critical for protecting payment endpoints)

- Simplifies client interactions by aggregating multiple service calls

- Provides a place for centralized logging, tracing headers, and security checks

Trade-offs & mitigations:

- Single point of failure: run the gateway highly available and instrument health checks.

- Latency and complexity: keep the gateway lightweight; avoid heavy business logic there.

- Security surface: ensure strong auth, RBAC checks, and telemetry.

Interview tip: Discuss how you’d implement per-client rate limits and throttling for payment APIs and how the gateway can enforce API quotas for third-party integrators.

5) Circuit Breaker (and Bulkhead)

What it is: Prevent cascading failures by failing fast when a dependency is unhealthy. Bulkheads isolate failures to a subset of resources.

Why use it in fintech:

- Protects core services from downstream outages (e.g., a card gateway or clearing partner)

- Improves overall system stability and predictable behavior under partial failures

Trade-offs & mitigations:

- Tuning: thresholds, timeouts, and reset intervals require careful tuning to avoid false positives.

- Complexity: you need fallback strategies (circuit open fallback, degraded mode, queued requests) and visibility into why circuits trip.

Interview tip: Explain how you’d combine circuit breakers with retries (exponential backoff), rate limits, and bulkheads. Mention libraries like resilience4j or patterns like token buckets for rate limiting.

Final checklist for interviews

When describing any pattern, cover these points succinctly:

- The problem the pattern solves

- Why it’s a good fit for fintech (consistency, audit, latency, compliance)

- Main trade-offs and failure modes

- How you’d monitor and recover (metrics: error rate, latency, queue depth; processes: reconciliation, alerting)

- A short example or past experience, if available

Mastering these patterns—and being able to explain the trade-offs and mitigations concisely—will help you stand out in fintech system design interviews.

If you want, I can convert this into a one-page interview cheat sheet or provide sample diagrams and answers for a payment-system design question.